You must have come across the term IRDA while reading about insurance related news and regulations.

India’s insurance industry is thriving and there is no dearth of providers offering different types of insurance, be it life, general, or specialized. But which agency makes sure that insurance companies operate fairly and follow best practices? That’s IRDA for you.

But what exactly is IRDA? Many are unaware of its functions, role, and overarching importance within the insurance sector. In this blog, Aapka Policywala will dive deeper into these aspects!

We bet that by the end, you’ll be equipped with a comprehensive understanding of IRDA and its impact. You’ll be able to pave your way through the insurance jungle with confidence.

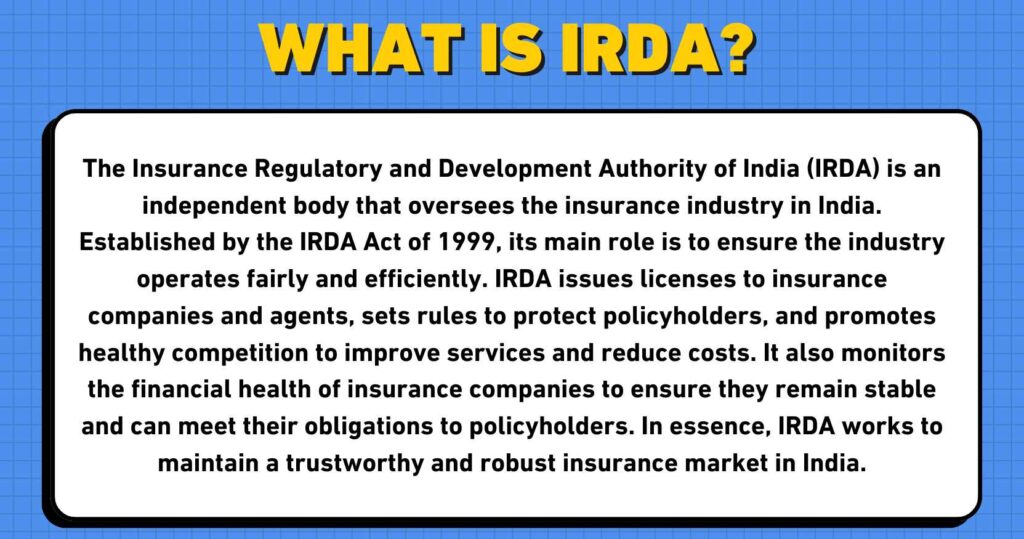

What is IRDA?

IRDA stands for Insurance Regulatory and Development Authority of India. Established in 1999, it’s the apex body that is tasked with overseeing and regulating the entire insurance sector in India. It makes sure that the industry functions smoothly. Also, that it promotes orderly growth and protects the interests of policyholders.

IRDA’s ambit encompasses all insurance companies operating in India. Happen to offer life insurance? Covered. General insurance? Covered. Other specialized products? Covered. By setting and enforcing regulations it works to guarantee fair competition, transparency, and financial stability within the insurance market.

What are the Functions of IRDA?

Alright, so you may have a good idea now about how IRDA plays the role of a guardian for India’s insurance firms. But what does this actually involve? Let’s take a closer look at these through its major functions which include:

- Safeguarding policyholder interests: IRDA’s primary mission is to protect the rights of policyholders. How does it do its duty? By ensuring that companies offer fair terms and conditions in their insurance products. Also, that they handle claims efficiently while maintaining transparency in their dealings.

IRDA empowers policyholders by setting grievance redressal mechanisms. This allows people to voice concerns and seek resolution if needed.

- Regulating industry with a fair hand: If you believe insurance companies to be cricket players, then IRDA is their umpire; it establishes regulations that oversee the behavior of insurance firms, including areas such as product development, pricing strategies, and marketing practices — among others — that would not be left within the discretion of the insurers.

- Promoting financial stability: Apart from regulating the insurance industry, IRDA also secures its financial health. It sets capital adequacy norms for insurance companies, making certain they have sufficient reserves to meet their obligations to policyholders.

This financial prudence protects policyholders from situations where a company might be unable to pay out claims due to insufficient funds.

- Promoting growth and development: The role of IRDA extends beyond just regulation. It actively works towards the orderly growth of the insurance sector of India. How, you ask? Firstly, it promotes financial inclusion by encouraging the development of accessible and affordable insurance products for the underserved population.

Moreover, IRDA fosters innovation within the industry by encouraging the development of new and relevant insurance that can cater to the evolving needs of policyholders.

A comprehensive guide on cash surrender value!

What are IRDA’s New Guidelines for Insurance Companies?

Finally comes the moment you all have been waiting for, “What are new guidelines introduced by IRDA to help insurance companies stay current and handle emerging challenges?” Well, here are some key updates:

1 Ensuring KYC Compliance

Back in 2023, IRDA established a rule that asks individuals to comply with Know Your Customer (KYC) guidelines. They are supposed to submit KYC documents when purchasing any new insurance policies. This new requirement applies to different types of insurance (including health, auto, travel, and home insurance).

What does this mean:

- Documents to submit: When buying a new policy, buyers must provide proof of identity, address, and sometimes photograph. Put simply, this regulation boosts security for policyholders.

- Purpose: By doing so, insurance companies can easily verify who you are. Not only does it help them maintain accurate records but also reduces fraud risks like identity theft and money laundering.

2 Regulation 31 of IRDA

Next up, we have Regulation 31. This rule focuses on ensuring robust internal systems within insurance brokerage firms. It moves heaven and earth to protect policyholder interests. Also, to promote transparency in the industry.

- Adequate internal systems: As we said earlier, brokers will be required to create structures, processes, and controls that can help them manage their operations, risks, and compliance fruitfully. It encompasses management of governance, risk management, compliance, IT, human resources, and customer service.

- Business assessment: Brokers must assess their business to determine the appropriate level of internal systems. Factors to consider? Number of employees, transaction volume and complexity, types of insurance products, geographical operations, and specific business risks.

- Implementation: Based on assessment, brokers should design and implement systems that address these factors adequately.

Learn everything about critical illness insurance plans in India.

Focus areas:

- Data management: Insurance companies must have robust systems for storing and securing data, processing, and protection. This includes:

- Safeguarding sensitive customer information

- Maintaining data backups

- Implementing cybersecurity measures

- Complying with data protection laws

- Risk management: Effective risk management systems are pivotal. Brokers must:

- Identify, assess, and manage operational risks

- Implement risk mitigation strategies

- Monitor risk exposure

- Create contingency plans to minimize disruptions

- Compliance: Brokers must check if they are following all relevant laws, regulations, and code of conduct

IRDA and Its New Guidelines: Final Words

There you go!

We told you everything important about IRDA a.k.a superhero of the insurance industry. By adhering to the new guidelines listed above, insurance companies can achieve several key benefits. They can strengthen their transparency; minimize fraud risks; build trust with policyholders. You can contribute to a more secure, reliable, and future-proof insurance ecosystem for everyone.

Are you someone who just happened to come across this blog and now wants to buy an insurance policy? Aapka Policywala can help you with that! We are a one-stop-shop platform where you can compare and choose from policies offered by different companies.

Got any queries to ask? Send them to info@aapkapolicywala.com. Our PSOP agents will be more than happy to answer them for you!

Check out these pages as well: