Insurance policies are long-term commitments that bring a lot of jargon and conditions. Surrender value is one such aspect of insurance policy that often baffles individuals, couples, and families alike.

To be fair, surrender value is a complex concept that requires a simple explanation. That’s why Aapka Policywala – a leading life insurance service provider in India – decided to list out everything crucial about surrender value.

Let’s get started!

Meaning of Surrender Value

In a life insurance policy, surrender value is the amount that is payable by the insurer to the policyholder if the policy is terminated before maturity. Insurance service providers charge a surrender fee (also known as a discontinuance charge) for premature termination of the policy. This amount may vary from company to company.

In simple words “ the Surrender value of an insurance policy is the amount that an insurance company will give you back when you terminate your insurance policy before the maturity period”

Surrender value ensures that you will get a part of your premium amount back as a lump sum. This surrender value factor depends on the percentage of premiums paid by you.

Misconception about policy surrender

One common misconception of insurance policy is it can’t be terminated. Let us tell you that it is official under a directive issued by the Insurance Regulatory Development Authority (IRDA), term plans in India provide the option to give up on your policy at any time.

The benefits, all rights, and interests linked with it will cease to exist, once you have decided to take off the insurance plan before its maturity. But you will be paid back the surrender value that your policy has accumulated over the years.

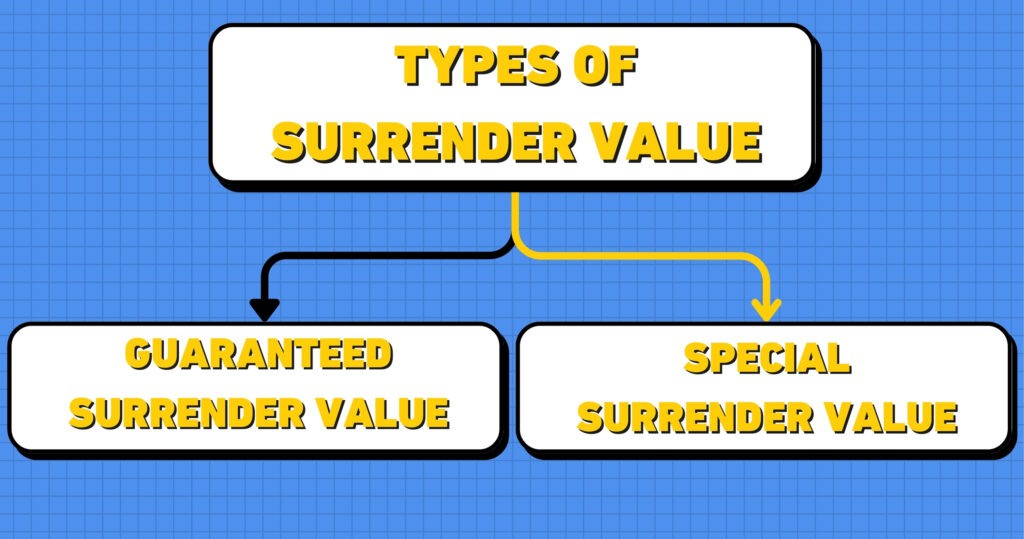

Types of Surrender Value

There are 2 Surrender Values: Meaning, Types, and FAQs which are as follows:

- Guaranteed Surrender Value

- Special Surrender Value

Let’s have a look at each of these in detail.

Guaranteed Surrender Value (GSV)

Guaranteed surrender value is the total money which is payable by the insurance company in the case of surrendering the insurance policy before its completion of maturity. In simple words, it’s the amount provided after policy cancellation. Its evaluation depends upon the value factor in the policy document. The surrender value factor lies in the percentage of the total premiums paid. When the insurance is close to its maturity period, the surrender value factor will almost be equal to 100% of the premiums paid.

In the policy brochure, this value is clearly stated in the documentation. You will get the sum of the premiums that you have paid for three years in a row. The sum is equivalent to all premiums paid up to this amount. Extra benefits, premiums for riders, and any bonus money (received upon maturity) are not included in the surrendered value of the policy.

Guaranteed surrender value= Premiums paid * Surrender value factor

Special Surrender Value (SSV)

It basically depends on several factors which include the total sum assured, total premiums paid, policy term, and applicable bonuses. The SSV may be higher or lower than the GSV depending on the policy’s terms and prevailing economic conditions.

To understand this, it’s important to delve into the concept of paid-up policy.

When a person is unable to pay the premiums, the insurance policy automatically converts into a paid-up policy. If you want to surrender a paid-up life insurance, the policyholder will receive a special surrender value.

The Special Surrender Value (SSV) of a life insurance policy is typically calculated using the formula:

Special Surrender Value = (Paid-up value + accrued bonuses) * surrender value factor

Here:

- The Paid-up value is calculated as the Basic Sum Assured multiplied by the ratio of the number of premiums paid to the total number of premiums payable.

- Accrued bonuses refer to any bonuses earned and added to the policy over its duration.

- The surrender value factor is a factor determined by the insurance company based on various policy-specific factors and prevailing market conditions.

Surrender Value FAQs

What Happens on Surrendering a Life Insurance Policy?

With the understanding of what a surrender value is, we can conclude that even if you have to terminate your insurance plan, still, you are bound to get a sum of money back. The insurance company will reimburse with the amount placed aside for savings plus additional interest. This is only possible if your insurance plan is accessible to provide a maturity value.

Here are important implications when you surrender a life insurance policy with a maturity value:

- The insurer receives the surrendered amount.

- Coverage ceases immediately upon surrender.

- Surrendering the policy means you cannot revive it in the future.

- All benefits associated with the policy cease to be in effect.

Do All Life Insurance Policies Offer Surrender Value?

Before surrendering an insurance policy, it is important to go through the list of terms and conditions. Most insurance providers in India have different policies regarding surrender value. By going through the paperwork, you will be able to analyze the minimum period for which the premiums are required to be paid before you can surrender the policy.

Policies like term insurance plans do not provide any compensation or surrender value if you decide to cancel the policy in the middle of the term. However, for insurance plans like Unit-Linked Insurance Plans (ULIPs) and Endowment Plans, you will receive a surrender value provided that you have paid your premiums for at least three years.

Is it wise to surrender an insurance policy?

If you decide to surrender your insurance plan, you will lose all the benefits of the policy and the amount you will receive could be much less than the premiums you have already paid. It’s essential to carefully evaluate your current financial situation and future needs before making this decision, as surrendering may only sometimes be the most advantageous option in the long run.

We advise surrendering only when the money is required to double your investments, generate higher returns, life-critical emergencies, or invest in another product.

Surrender Value: Final Words

Remember, insurance policies are designed to provide long-term financial security. Therefore, it’s essential to weigh the benefits and drawbacks of surrendering against your broader financial goals before making a final decision. However, once you surrender your insurance plan, there’s no way to go back. You will get the lump sum amount but lose the long-term benefits.

Still have queries to ask about surrender value? Leave them in the comments and get a quick reply from the insurance experts.

Have a look at our insurance plans: